Beyond Hormuz: The Pipelines That Try to Replace the World’s Most Important Oil Chokepoint

What This Means for Indian Navy SLOC Protection

Pipelines help the system absorb shocks. Yet the geography of global oil trade still revolves around a narrow channel between Iran and Oman.

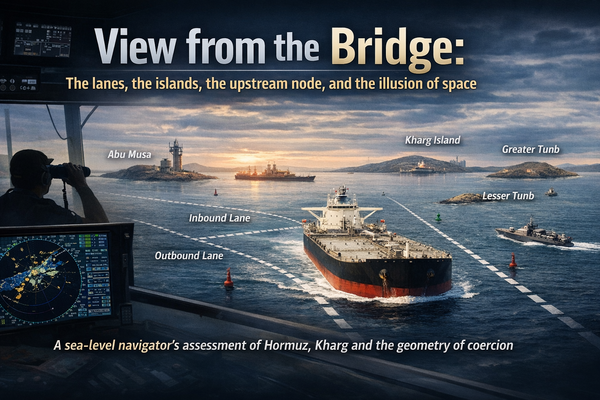

Few places on earth matter as much to the global energy system as the Strait of Hormuz.

This narrow waterway between Iran and Oman is the exit gate for the Persian Gulf. In practice, tankers carrying crude from Saudi Arabia, Iraq, Kuwait, Qatar, the UAE and Iran almost all pass through it to reach global markets.

Under normal conditions, roughly 20 million barrels per day of oil and petroleum liquids move through the strait—close to one-fifth of the world’s seaborne oil trade. On top of this oil traffic, roughly one‑fifth of global LNG trade also passes through Hormuz, further concentrating both oil and gas risk in the same narrow stretch of water. Because of this concentration, Hormuz has long been the world's most important energy chokepoint. Any disruption immediately raises fears of supply shortages, shipping delays and price spikes.

Whenever tensions rise in the Gulf, analysts ask the same question: if Hormuz becomes unsafe or blocked, can exporters bypass it?

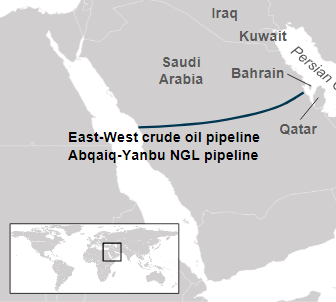

Several pipelines and alternative routes exist. Saudi Arabia can send crude west to the Red Sea. The UAE can export from Fujairah outside the Gulf. Iraq has a Mediterranean outlet through Turkey. Egypt operates the SUMED pipeline, which links the Red Sea and the Mediterranean.

These routes help. But none can replace the scale or efficiency of Hormuz.

Understanding why requires examining the geography, capacity, and vulnerabilities of each alternative.

Thanks for reading नीतिविद्या | Nitividya – Strategy, Institutions, Power! This post is public so feel free to share it.

Saudi Arabia’s westward escape: the Yanbu route

The most significant bypass is Saudi Arabia’s East–West Pipeline, commonly called Petroline.

Built in the early 1980s during the Iran–Iraq War, it was designed to provide an export route that avoided Hormuz entirely. The pipeline runs about 1,200 kilometres across Saudi Arabia from Abqaiq in the eastern oil fields to the Red Sea port of Yanbu, via two giant 48‑ and 56‑inch lines.

Key capabilities:

Standard capacity: about 5 million barrels per day

Surge capability: up to roughly 7 million barrels per day when additional lines are repurposed

Endpoint: Yanbu Industrial Port on the Red Sea

In a crisis, Saudi Aramco can increase flows through Petroline and load tankers on the Red Sea rather than the Persian Gulf. For Asian buyers including India, this provides a partial hedge against disruption in the Gulf.

Saudi Aramco has invested in expanding the East–West Pipeline beyond its original 5 million bpd design, with company documents indicating sustainable flows above 6 million bpd and temporary surges up to around 7 million bpd in crisis conditions.

But two limitations quickly appear.

Terminal constraints

The Yanbu export complex has historically loaded well under 2 million barrels per day, making the port itself the bottleneck rather than the pipeline. Even if Saudi Arabia pushes Petroline close to design capacity, tanker loading limits restrict how much oil can actually leave the Red Sea.

New maritime risks

Rerouting oil westward does not eliminate the risk of chokepoints. Tankers leaving Yanbu must pass through the Bab el‑Mandeb Strait, which connects the Red Sea to the Gulf of Aden.

In recent years this corridor has become increasingly dangerous due to missile and drone attacks on commercial vessels originating from Yemen’s Houthi movement.

The East–West line and related Saudi infrastructure have themselves been targeted; in 2019 a Houthi drone strike temporarily shut part of the pipeline, and strikes have hit energy and desalination facilities on the Red Sea coast, including near Yanbu and Jeddah.

The result is strategic substitution. Hormuz risk is replaced by Red Sea risk.

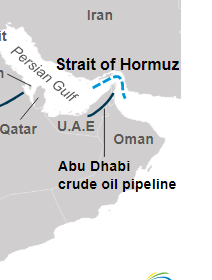

The UAE’s workaround: Fujairah pipeline

The United Arab Emirates built its own bypass for similar reasons.

The Habshan–Fujairah pipeline (ADCOP) moves crude from Abu Dhabi’s inland oil fields to the port of Fujairah on the Gulf of Oman. Unlike most UAE export terminals, Fujairah lies outside the Strait of Hormuz; tankers loading there do not need to transit the Gulf.

Key features:

Capacity: about 1.5 million barrels per day

Route: Habshan oil fields to Fujairah port

Strategic role: bypass Hormuz for part of UAE exports

Fujairah has also developed into a major bunkering and storage hub.

The pattern, however, is familiar. The pipeline covers only a portion of UAE output; much of the country’s crude still relies on Hormuz routes. Fujairah itself becomes a concentrated strategic node. In crisis conditions, attacks on export terminals, storage tanks or shipping lanes around the port could quickly disrupt flows.

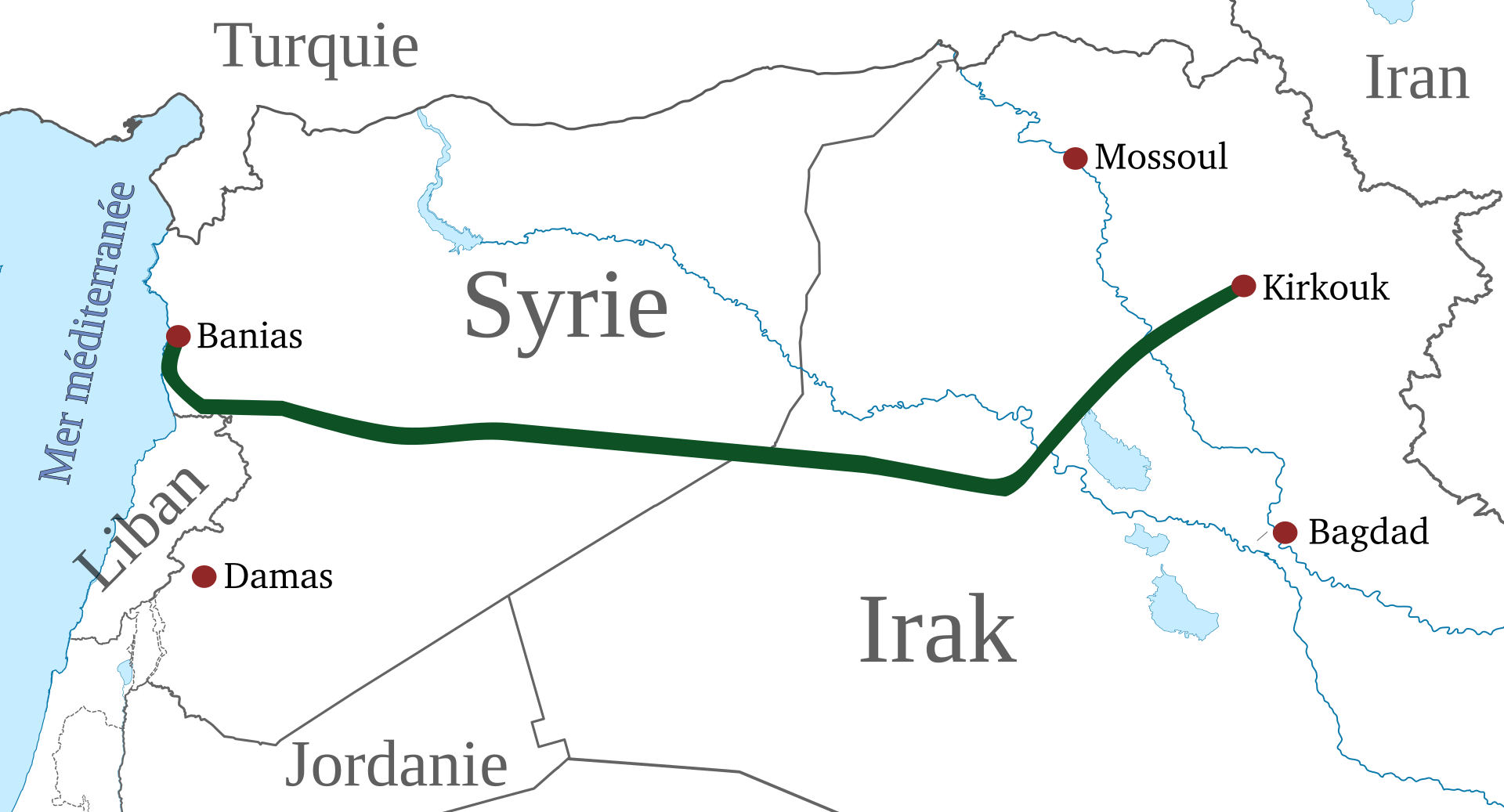

Iraq’s Mediterranean route: Kirkuk to Ceyhan

Iraq theoretically has the most direct Hormuz bypass.

The Kirkuk–Ceyhan pipeline connects oil fields in northern Iraq to the Turkish Mediterranean port of Ceyhan, allowing crude to reach global markets without entering the Persian Gulf.

In practice, this route has struggled with chronic disruptions:

Political disputes between Baghdad and the Kurdish authorities

Legal battles over transit and revenue sharing

Sabotage and security incidents along the line

As a result, flows have often operated far below design capacity and have been completely halted for extended periods.

Strategically, this makes the route unreliable as a crisis‑time pressure valve.

Egypt’s SUMED pipeline

The SUMED pipeline in Egypt plays a different role.

It runs from Ain Sokhna on the Red Sea to Sidi Kerir on the Mediterranean, carrying crude across Egypt and bypassing the size limits of the Suez Canal, with capacity of roughly 2.5 million barrels per day.

SUMED does not allow oil to escape the Persian Gulf directly. Instead it moves oil that has already reached the Red Sea onwards to European markets. In a Hormuz crisis, SUMED would help manage logistics and congestion further west, but it does not change the fundamental vulnerability of Gulf exports at the strait.

Why bypass pipelines cannot replace Hormuz

Taken together, these routes look significant:

- Saudi Petroline

- UAE Habshan–Fujairah

- Iraq–Turkey pipeline

- Egypt’s SUMED

They represent several million barrels per day of potential diversion capacity.

Yet the gap between bypass capacity and Hormuz flows remains large. The Strait of Hormuz normally handles around 20 million barrels per day. Even if Saudi Arabia, the UAE and Iraq ran their bypass pipelines at or near full capacity and SUMED were fully utilised, they would still fall well short of replacing typical daily flows through the strait.

Each route also introduces its own vulnerabilities:

Limited port loading capacity

Dependence on politically unstable transit corridors

Infrastructure exposed to missiles or drones

Additional chokepoints such as Bab el‑Mandeb

The global oil system, therefore, remains structurally dependent on Hormuz.

Bypass routes reduce risk concentration; they do not eliminate it.

What Hormuz disruption means for India

For India, the implications are immediate and serious.

India imports over 85 percent of its crude oil, and the Middle East is its largest supplier. Saudi Arabia, Iraq, the UAE, and Kuwait collectively account for a major share of those imports. Most shipments transit Hormuz before crossing the Arabian Sea to India’s western coast.

Unlike crude, LNG has no overland escape from Hormuz. It travels almost entirely by ship, which means India’s gas and oil security both live or die on the same vulnerable sea‑lanes.

Unlike crude, there is no equivalent overland pipeline network for LNG cargoes to bypass Hormuz. LNG moves almost entirely by specialised carriers from liquefaction plants to importing terminals. That leaves the global gas trade locked into a small number of deep‑water sea lanes and chokepoints. For India, where more than half of LNG imports come from Qatar and the UAE via the Strait of Hormuz, this leaves LNG security just as exposed to maritime disruption as oil.

These flows sit on top of other critical sea‑lines of communication that link the Indian Ocean to East Asia, above all through the Strait of Malacca; together they form the maritime backbone of India’s energy and trade security. Hormuz is simply the most concentrated and vulnerable point in this wider network, which is why it is a useful case in point for thinking about India’s SLOC protection problem as a whole.

A disruption would affect India through three main channels.

1. Naval and maritime security pressure

The Indian Navy already maintains a strong presence in the Arabian Sea and western Indian Ocean. If shipping through Hormuz were threatened, naval tasks would expand quickly into:

Escort operations for Indian‑flagged tankers

Maritime surveillance along key sea lanes

Cooperation with multinational task forces

Protection of Indian merchant vessels in high‑risk zones

Such missions are resource‑intensive and stretch assets from the Gulf to the Red Sea. Sustaining them at scale and over time demands a larger, better‑resourced Indian Navy, not just temporary redeployment.

In wartime, the picture becomes even more complicated. Submarines hunting tankers and their escorts in confined waters would turn Hormuz, the Gulf of Oman and the approaches to Bab el‑Mandeb into contested kill zones, where detection is difficult and reaction time is short. Carrier groups, surface combatants and long‑range maritime patrol aircraft can reduce the risk, but they cannot make sea‑lanes invisible to modern torpedoes and anti‑ship missiles. For India, that translates into a long‑term requirement for credible undersea warfare capability and robust anti‑submarine warfare forces at sea and in the air.

2. Shipping insurance and freight costs

Even if tankers continue sailing, insurance markets react rapidly to risk. When corridors become dangerous, insurers impose war‑risk premiums on vessels entering those waters. Past crises have seen these premiums surge, adding hundreds of thousands of dollars to a single voyage.

If ships detour around the Cape of Good Hope instead of the Red Sea, transit times increase by roughly 10–15 days, raising fuel consumption and reducing the number of voyages per ship. The combined effect is a sharp increase in freight costs for oil deliveries to Asia.

3. Oil price shocks

Even partial disruption in Hormuz would tighten supply expectations and push oil prices higher. Because crude is traded globally, India cannot insulate itself from such shocks even if some imports arrive via alternate routes.

Higher crude prices quickly translate into:

Rising import bills

Currency pressure

Inflation risks

Energy security thus becomes both an economic and strategic issue.

The strategic lesson

Pipelines such as Petroline or the Habshan–Fujairah route are often described as Hormuz bypasses. In reality, they function more like pressure‑relief valves.

They allow exporters to redirect part of their output during crises and give importers some flexibility in where cargoes are loaded. But they cannot replicate the Strait of Hormuz’s scale.

For India and other Asian energy importers, the real answer lies not in a single bypass but in a portfolio strategy:

Diversified suppliers beyond the Gulf

Flexible lift points such as Yanbu and Fujairah

A stronger, persistently deployed Indian Navy in the Indian Ocean

Robust strategic petroleum reserves

The Strait of Hormuz remains the centre of gravity of the world’s energy supply. This geography translates directly into a long‑term requirement for New Delhi: investing in a navy capable of protecting sea‑lanes across the wider Indian Ocean’s SLOC network, whatever pipelines are built ashore, and shaping defence budgets and force‑structure choices around this fact.