Hormuz and the Financial Spine of Maritime Trade

How insurance, reinsurance and global risk capital can close vital sea lanes even before a shot is fired

Recent analysis by Shanaka Anslem Perera1 suggests that the recent disruption in tanker traffic through the Strait of Hormuz may have been triggered not primarily by mines or missiles, but by withdrawals of maritime insurance. Modern maritime trade runs on financial guarantees as much as on naval security.

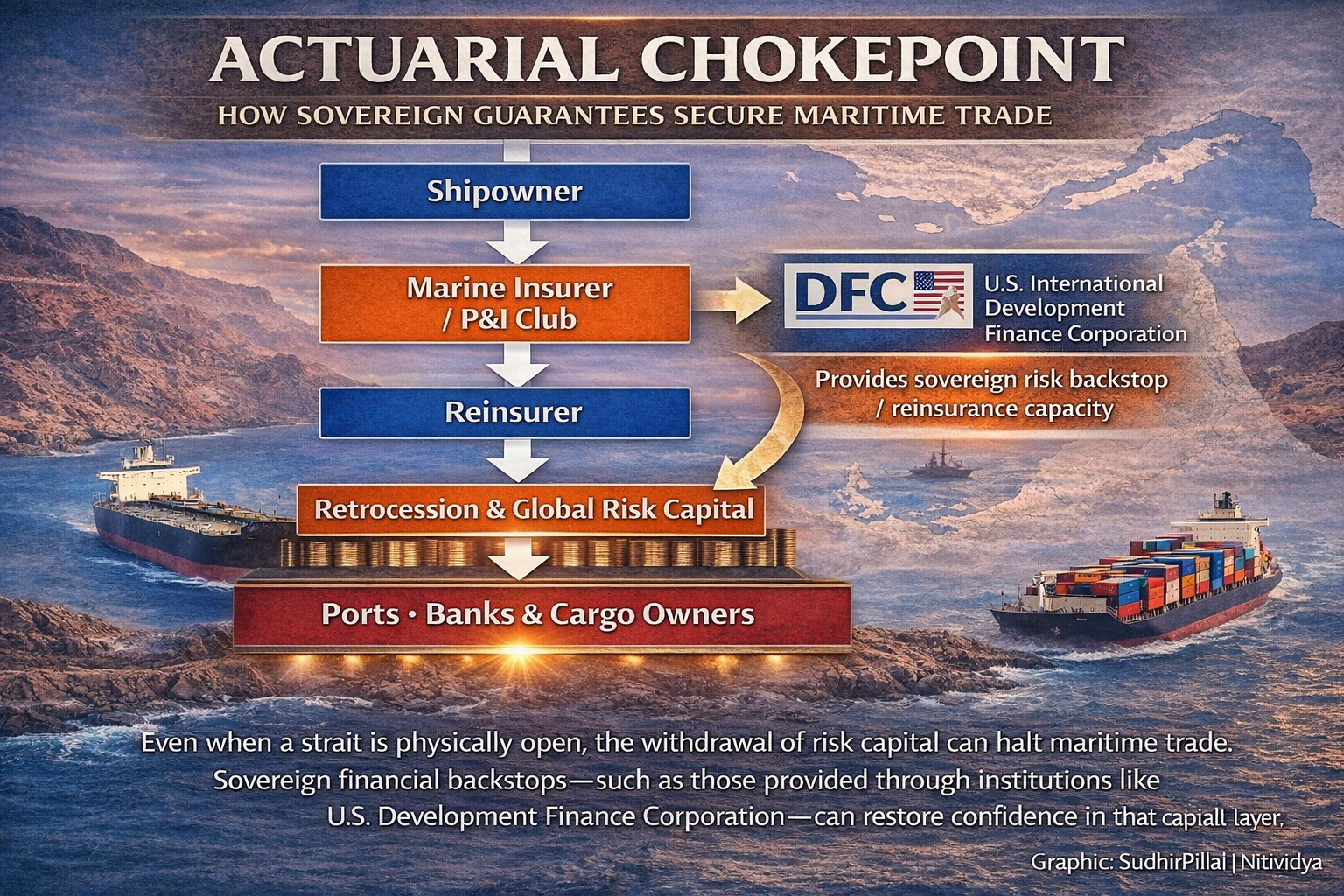

The Insurance Mechanism Behind Global Shipping

Modern shipping does not move on steel and fuel alone. It moves on a stack of financial assurances that make voyages commercially acceptable. At its simplest, the architecture looks like the graphic above.

Each layer relies on the one above it in the risk chain.

If reinsurers withdraw, insurers tighten coverage.

If insurers tighten coverage, shipowners cannot obtain acceptable insurance certificates.

If certificates disappear, ports, banks and charterers refuse to handle the voyage.

At that point, the ship may still be physically seaworthy, but it becomes commercially unusable.

This is why Perera argues that seven insurance notices achieved what naval action had not: they turned the Strait into a commercially closed corridor.

Why P&I Clubs Matter

Protection & Indemnity (P&I) clubs2 are not conventional insurers.

They are mutual associations owned by shipowners. Members pool liabilities collectively, catastrophic losses ultimately fall back on the membership, and the clubs rely heavily on reinsurance markets to absorb extreme risks.

When the tail risk of a war zone becomes impossible to model, reinsurers step back. Once that happens, P&I clubs must rapidly tighten or withdraw cover.

This is how the market can freeze in hours — even before major physical losses occur.

The Redundancy Problem

One might assume that if some insurers withdraw, others simply step in.

In practice, redundancy is limited.

Concentration of risk capital. Marine insurance and reinsurance are clustered in a few global hubs.

Shared exposure models. When risk models change, they tend to change for everyone at once.

Tail-risk constraints. Even a single tanker loss can generate enormous liabilities.

As a result, the market can harden almost synchronously. This is why Perera describes the episode as an “actuarial blockade.”

The Insurance Loop Behind the Hormuz Crisis

At first glance, the Hormuz insurance crisis appears to follow a neat four-step loop: insurers withdraw capacity, Washington offers a sovereign backstop, confidence returns, and shipping resumes. That is the story embedded in many press releases and podium statements.

In reality, the system operates through five distinct layers, each with its own constraints.

1. Shipowners need insurance before they can sail

Commercial vessels cannot simply depart port on the captain’s judgment.

To operate legally and commercially, they must carry valid insurance certificates. These are required by: ports, canal authorities, banks financing the cargo, and charterers hiring the vessel.

Without those certificates, the voyage cannot proceed even if the sea lane itself is physically open.

2. Marine insurers and P&I clubs provide the first layer of cover

Shipowners obtain coverage primarily through:

Marine insurers (for hull damage)

P&I clubs (for pollution, crew injury and liability risks).

These organisations pool risk across thousands of vessels. However, their balance sheets cannot absorb very large catastrophic losses.

That is why they rely on a second layer.

3. Reinsurers absorb catastrophic risk

Marine insurers transfer large portions of their exposure to reinsurance markets.

Reinsurers provide capital that protects insurers against extreme losses, such as the destruction of multiple vessels, large environmental spills, and cascading wartime incidents. If reinsurers judge the risk environment unacceptable, they may: raise premiums sharply, limit coverage, and withdraw capacity entirely.

When that happens, the insurers below them must immediately tighten their own coverage.

4. The retrocession layer spreads risk even further

Reinsurers themselves rarely hold the entire risk. They spread it again through what is known as retrocession.

This moves risk into a broader capital pool that includes: other reinsurers, specialist retrocession funds, catastrophe bond investors, and insurance-linked securities. This upper layer is where the global insurance system ultimately reaches its capital limits.

If that capital withdraws, the entire insurance stack below it becomes unstable.

Enter the US Development Finance Corporation

Recognising that the immediate constraint was financial rather than naval, the United States responded not with additional warships but with a balance-sheet instrument.

The US International Development Finance Corporation (DFC) announced an emergency reinsurance backstop intended to support Gulf shipping. Such facilities attempt to provide sovereign guarantees, emergency reinsurance capacity, and political risk coverage.

The goal is to convince insurers that catastrophic losses will not destroy their balance sheets. Diagrammatically, this would look something like this.

What the Diagram Does Not Show

However, sovereign announcements alone do not reopen the market. Insurers require contractual clarity on scope, first-loss provisions, sanctions exposure and duration before capacity returns.

The diagram captures the surface narrative, but the reality is more complex. Insurance markets need time to rebuild risk models, re-underwrite vessels, and determine premiums the market will tolerate. Each arrow in the diagram hides a deeper structural process.

From “catastrophic loss” to model breakdown

The issue is not simply that insurers become nervous. War-risk underwriting relies on probabilistic loss estimates. When conflict risk becomes open-ended — multiple vessels, pollution liabilities, escalation across ports — actuarial models stop producing stable probabilities.

Two effects follow: regulatory capital stress, as insurers must hold capital against worst-case scenarios; and board-level risk decisions, in which underwriting desks are instructed to withdraw or restrict cover.

From “sovereign backstop” to contested credibility

A government backstop, a sovereign guarantee mechanism designed to unlock private capital rather than a programme of direct government funding, does not automatically restore capacity. Markets ask technical questions:

What risks are covered?

What is the legal instrument — guarantee, indemnity, or reinsurance treaty?

How does it interact with sanctions regimes?

Who absorbs the first loss?

How long does the facility remain open?

Until these details are written into binding contracts, the backstop remains largely a policy signal rather than deployable risk capital.

From “shipping resumes” to selective reopening

Even when insurance begins to return, trade rarely restarts evenly.

Coverage reappears in layers: certain vessel flags regain cover first, specific owners or charterers secure better terms, routes deemed safer reopen earlier, and politically sensitive cargoes face tighter conditions.

For India, this differentiation matters. VLCC crude flows may normalise relatively early, while LNG or fertiliser feedstocks can remain saddled with higher premia or limited capacity.

The result is not an instant reopening of Hormuz, but a gradual and uneven restoration of commercial confidence.

Hormuz Is Not Only About Oil

Oil dominates the headlines, but it is only part of the story.

Hormuz also carries: LNG from Qatar, petrochemical feedstocks, and fertilisers such as ammonia and urea.

Fertiliser exports are particularly important for India, Brazil and much of Southeast Asia. Disruptions at Hormuz can therefore surface months later as agricultural price shocks, not just energy inflation.

India’s Strategic Options

India sits downstream of several of these flows. A large share of its crude imports comes from Gulf producers. It also depends heavily on fertiliser inputs sourced from the same region. War-risk premiums increase freight costs across all commodities.

Even if India remains outside the conflict, the insurance system can transmit disruption into the Indian economy with very little warning.

Possible responses include:

Diversifying supply. India has already expanded purchases of Russian crude, which can act as a buffer when Gulf supply is disrupted.

Expanding alternate sourcing. West Africa, the United States and Latin America provide alternatives, though often at higher transport costs.

Building strategic reserves. Larger energy and fertiliser stockpiles provide short-term protection against shipping disruptions.

Strengthening maritime finance. The deeper strategic question is whether India should build its own ecosystem for marine insurance, reinsurance, shipping finance and maritime arbitration. Initiatives such as GIFT City point in this direction.

The Strategic Lesson

The Hormuz episode illustrates a broader shift in maritime power.

In earlier eras, controlling a chokepoint meant deploying fleets. Today, financial infrastructure — insurance, reinsurance and risk capital — forms an equally decisive layer of control.

A strait may be physically open and yet commercially closed.

For India, the implication is clear. Maritime strategy can no longer stop at warships and chokepoints. It must extend to the financial architecture of shipping itself: insurance depth, reinsurance capacity, shipping finance and credible maritime legal frameworks.

Russian oil, alternative suppliers and strategic reserves can cushion shocks, but they remain tactical buffers.

The strategic objective must be broader: ensuring that in a crisis, the decision on whether Indian commerce sails is not determined solely in distant underwriting rooms, but within a maritime system in which India itself is a consequential participant.

For a detailed analytical treatment, see Shanaka Anslem Perera’s essay “Actuarial Warfare: How Seven Insurance Letters Closed the World’s Most Critical Chokepoint.” ↩

China has built out substantial domestic maritime insurance capacity but remains tightly exposed to the same London‑centred reinsurance system as everyone else. Chinese shipowners increasingly use the China Shipowners Mutual Assurance Association and state insurers such as PICC; these maintain extensive commercial relationships and shared reinsurance markets with the International Group of P&I Clubs, even though China P&I itself sits outside the IG pooling agreement. Since the current crisis began, Iran has still managed to send roughly 12 million barrels of crude through the Strait of Hormuz, almost entirely destined for China, often on sanctioned or “dark” tonnage operating under bespoke political understandings rather than standard IG‑backed war‑risk cover. Naval escorts and political deals may therefore keep some Chinese‑linked tankers moving in places like Hormuz, but the wider economic viability of Chinese shipping and mainstream Chinese‑owned fleets still rests on access to liability cover and war‑risk capacity that is ultimately constrained by global — largely London‑brokered — insurance and reinsurance markets.