The AMCA Programme: How India Tweaked the Developmental Model

Why HAL Appears to Have Been Excluded from the Prototype Development Phase

Origins and the Traditional Approach

The Advanced Medium Combat Aircraft (AMCA) has been India’s most ambitious indigenous combat aviation programme since its conceptualisation in the early 2000s. Designed by the Aeronautical Development Agency (ADA) under DRDO, the AMCA is envisioned as a 25–27 tonne, twin-engine, fifth-generation stealth multirole fighter with internal weapons bays, sensor fusion, AI-assisted mission systems, and supercruise capability. The Indian Air Force (IAF) is expected to induct approximately 126 aircraft (seven squadrons), with two variants — the Mk1 powered by GE F-414 engines and the Mk2 with a co-developed high-thrust engine (possibly the Safran deal, which is before the Cabinet Committee on Security (CCS).

The programme’s journey from concept to its current inflection point has been defined by repeated shifts in the industrial execution model. Understanding these shifts is essential to grasping why Hindustan Aeronautics Limited (HAL) — India’s sole fighter manufacturer for decades — now apparently finds itself excluded from the prototype development phase.

Phase 1: The Original SPV Model (2020–2024) — HAL-Led, Private Minority

When the AMCA programme was first given shape as a formal development project around 2020, the Ministry of Defence proposed a Special Purpose Vehicle (SPV) framework. Under this model:

– HAL would manufacture the first 40 AMCA Mk1 jets in the initial production phase, leveraging its existing fighter manufacturing infrastructure (Nashik, Bengaluru).

– A private sector company would hold a majority stake in the SPV and take over production of the AMCA Mk2 — the more advanced variant intended for the bulk of the 120+ aircraft order.

– ADA would remain the design authority, while HAL and the private partner would jointly execute development and production.

This was an unprecedented structure for Indian defence — the first time a private company was to hold majority ownership in a combat aircraft production entity. The rationale was sound: bring in private sector efficiency, capital, and manufacturing agility alongside HAL’s institutional aerospace knowledge.

Why the SPV Model Collapsed

The SPV model stalled for over three-and-a-half years, with no private partner coming forward. Former IAF Chief ACM R.K.S. Bhadauria (Retd.), who was in office when the model was proposed, publicly confirmed in a January 2024 interview to Livefist that “initial discussions on this have not gone well”.

The reasons were structural:

– Profitability concerns: Private companies were expected to invest in setting up an entirely new production line (initially planned for Coimbatore under the Tamil Nadu Defence Industrial Corridor), manage the entire supply chain from raw materials to final assembly, and bear significant financial risk — all for an aircraft that was not expected to enter series production until 2035 at the earliest.

– Order book uncertainty: The SPV’s financial viability depended on guaranteed government orders. With the Mk2 timeline linked to the yet-to-be-finalised engine deal, private firms had no clarity on when revenue would flow.

– Risk asymmetry: HAL had guaranteed revenues from its massive existing order book (Tejas Mk1A, Su-30MKI, helicopters), while the private partner would be making a bet-the-company investment on an untested programme.

ACM Bhadauria noted that ADA’s engagement with industry had been “preliminary in nature, an explorative kind of discussion” rather than serious partnering negotiations.

Phase 2: The “Development-cum-Production Partner” (DcPP) Interim Concept

As the SPV model floundered, the MoD briefly considered a dual-prototype DcPP model — funding both HAL and a private company to independently develop AMCA prototypes, with minor system variations, followed by competitive evaluation. The better-performing aircraft would win the bulk of the production order, potentially in a 60:40 split between the two companies.

This model was designed to:

– Mitigate risk by maintaining two production lines

– Inject genuine competition

– Avoid single-point-of-failure dependence on either HAL or a private entity

However, this concept too was overtaken by a more decisive policy shift.

Phase 3: The Programme Execution Model — Competitive Bidding (May 2025)

On 26 May 2025, Defence Minister Rajnath Singh approved the AMCA Programme Execution Model, which represented the most radical departure yet from India’s traditional defence procurement approach.

The key features of this model:

– Competitive, merit-based selection replacing the nomination-based system under which HAL historically received all fighter programmes without contest.

– Open bidding to Indian companies — public or private — independently, as joint ventures, or as consortia.

– ADA as lead executing agency, partnering with the selected entity (not HAL by default) for prototype development.

– Evaluation via a Combined Quality-cum-Cost Based System (CQCCBS), assessing technical competence, manufacturing capacity, financial strength, and timeline adherence.

Defence Secretary Rajesh Kumar Singh articulated the policy shift explicitly: “Whether it is the AMCA, which is a developmental model, or standard shipbuilding contracts, these will no longer be awarded through nomination. They will be tendered to ensure genuine price discovery and fair competition“.

This was a deliberate break from decades of HAL’s monopoly in fighter aircraft manufacturing — philosophically aligned with the broader Atmanirbhar Bharat push, but operationally designed to bring private-sector speed and accountability to a programme India cannot afford to delay.

Procedurally, this represented a departure from established acquisition norms:

– The AMCA programme is categorised as a Make-I project under Chapter III of the Defence Acquisition Procedure (DAP) 2020, with government funding for prototype development.

– However, as a DRDO-designed system, it also falls under Chapter IV of DAP 2020, which governs acquisition of systems designed and developed by DRDO/DPSUs.

– Under standard Chapter IV procedure, DRDO — through ADA — would ordinarily nominate a Development-cum-Production Partner (DcPP) through its internal processes, which historically defaulted to HAL without competitive bidding. This was the model followed for the LCA Tejas, LCH Prachand, and every other DRDO-designed combat platform.

– The May 2025 Programme Execution Model effectively overrode this nomination-based pathway in favour of competitive selection — grafting the open-bidding philosophy of the Make category onto what the DAP’s own framework would have permitted as a straightforward DRDO-to-HAL handoff.

The Expression of Interest: Criteria That Shaped the Outcome

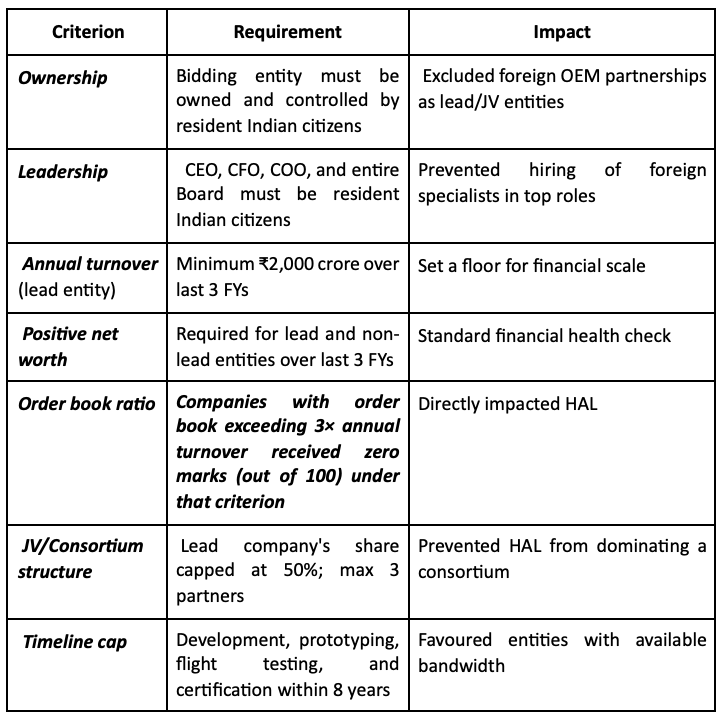

On 18 June 2025, ADA issued the Expression of Interest (EoI) for the AMCA Development Phase. The EoI contained several eligibility criteria and a point-based scoring system that would prove consequential.

The Ironic Twist: Both Sides Complained

Private companies initially alleged the process was rigged in HAL’s favour. Before the 4 July 2025 pre-EoI meeting, they argued that the stringent qualifying criteria — especially the requirement for fighter-class manufacturing experience, Indian-only ownership, and the bar on foreign OEM leadership — made it “nearly impossible” for any private company to compete independently against HAL’s decades of institutional experience.

HAL simultaneously argued that the criteria were loaded against it. HAL Chairman & Managing Director DK Sunil publicly stated in July 2025: “There are clauses that have loaded the dice against HAL. The EoI says if a company’s order book is three times its turnover, then it will get zero marks. In HAL’s case, it is almost 8×. It means someone who has fewer orders will get more marks. I don’t know why they have done this“.

This was a striking paradox: private companies thought HAL would inevitably win, while HAL’s own leadership saw defeat in the fine print.

The Evaluation and HAL’s Elimination (Late 2025 – February 2026)

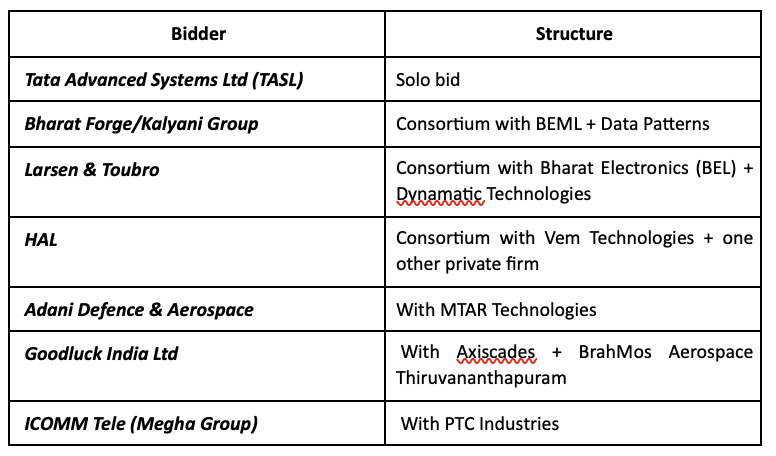

Seven bidders responded to the EoI by the 30 September 2025 deadline:

A high-powered evaluation committee chaired by former DRDO missile scientist Dr. A. Sivathanu Pillai assessed the bids on technical expertise, manufacturing capability, experience in development and testing, order book position, and financial strength. The findings were then reviewed by a panel chaired by Defence Secretary Rajesh Kumar Singh.

Result: Three Qualified, Four Eliminated

On 2 February 2026, Defence Secretary Rajesh Kumar Singh confirmed on the record that, of the seven consortia that submitted bids, three had cleared the pre-qualification stage and would receive the Request for Proposal (RFP) to submit cost bids for building five AMCA prototypes and one structural test specimen. He did not, however, publicly name either the qualified or eliminated entities.

Based on consistent, multi-source reporting by Hindustan Times, Economic Times, Moneycontrol, and CNBC-TV18 — attributed to officials familiar with the evaluation — the three qualified bidders are understood to be:

Qualified:

– Tata Advanced Systems Ltd (TASL)

– Kalyani/Bharat Forge consortium (with BEML and Data Patterns)

– Larsen & Toubro consortium (with BEL and Dynamatic Technologies)

Eliminated:

– HAL (with Vem Technologies)

– Adani Defence (with MTAR Technologies)

– Goodluck India (with Axiscades and BATL)

– ICOMM Tele/Megha (with PTC Industries)

HAL’s position: HAL issued a stock exchange clarification on 3 February 2026 stating that it had “not received any official communication in this regard“ and was therefore “not in a position to comment on these reports at this stage.” HAL CMD DK Sunil subsequently echoed this, calling the reports speculative — though notably, he did not deny the substance of the reporting. No formal notification from ADA or MoD listing the qualified or disqualified entities has been released as of this writing.

Why HAL Is Reported to Have Failed to Qualify

According to multiple reports, the central reason was the order book-to-turnover ratio criterion. HAL’s confirmed order book stood at approximately ₹2.52 lakh crore (₹2.52 trillion), while its FY25 turnover was approximately ₹30,105 crore. This gave HAL an order book-to-turnover ratio of over 8× — far exceeding the 3× threshold beyond which companies received zero marks under that scoring head.

What had always been presented as HAL’s greatest strength — a massive, multi-year confirmed order book giving revenue visibility until 2032 — was reportedly turned into its disqualification trigger. The policy logic, according to officials familiar with the process, was that the AMCA programme “demands focus, speed and the ability to absorb complex design and manufacturing work,” and a company already overwhelmed with a backlog eight times its annual capacity could not credibly commit dedicated bandwidth.

HAL also attempted to partner in a consortium structure, but even there, its dominant position and the associated financial metrics reportedly made qualification untenable under the scoring framework. HAL’s proposed JV model envisaged retaining a 50% stake while inducting private partners for specific airframe sections — but this structure could not overcome the underlying financial disqualification.

The Strategic Rationale: Deliberate or Incidental?

The question that defence watchers and HAL’s own leadership have raised is whether HAL’s exclusion was an incidental outcome of neutral criteria, or a deliberate policy design.

Several indicators suggest the latter:

– The order book clause was unusual. Standard defence procurement EoIs do not penalise companies for having large backlogs. In most contexts, a robust order book signals capability and credibility. The specific 3× threshold, with a zero-mark penalty, appears tailored to a situation where only one bidder — HAL — would fall foul of it.

– The broader policy shift was explicit. Defence Secretary Singh’s public statements about ending nomination-based contracts and the MoD’s declared intent to create competitive private sector participation in combat aircraft manufacturing indicate a conscious strategic direction.

– Tejas delivery delays provided the backdrop. The Tejas Mk1A delivery schedule has slipped repeatedly due to supply chain and GE F404 engine availability issues. HAL’s bandwidth was demonstrably stretched, giving officials a substantive (not merely procedural) basis for concern about adding another complex programme.

– The C-295 precedent. The award of the C-295 military transport aircraft manufacturing contract to TASL in partnership with Airbus had already broken HAL’s monopoly in fixed-wing military aircraft production. AMCA extends this to the fighter aircraft domain.

HAL CMD DK Sunil, while flagging the criteria publicly as early as July 2025, also acknowledged that the company would not be materially affected in financial terms, since AMCA prototype development was only worth ₹15,000 crore and HAL’s pipeline through 2032 (Tejas Mk1A, LCH Prachand, IMRH, LCA Mk2, CATS) remains robust. In effect, HAL’s leadership treated this as a strategic setback rather than an existential threat — but the symbolism is profound.

What Happens Next

The three shortlisted entities — TASL, Kalyani consortium, and L&T consortium — will now receive the RFP and submit cost proposals. The MoD expects to select the winning bidder within approximately three months, with contract award following after cost negotiations. The winning entity will partner with ADA to build five AMCA prototypes and one structural test specimen under the ₹15,000 crore allocation. The first flight is targeted for 2028–2029, certification by 2032, and series production from 2035.

HAL will likely retain a role — potentially holding a minority stake in the eventual production SPV — and will provide critical components (engines, landing gear), subsystem expertise, and institutional aerospace knowledge drawn from its Tejas and Su-30MKI experience. But it will not be the lead manufacturer. If the current reporting holds, this will mark the first time in the history of independent India that a private company serves as the prime contractor for a fighter aircraft programme.

Assessment

The AMCA model evolution — from HAL-led SPV (2020) to collapsed SPV (2020–2024) to competitive open bidding (May 2025) to HAL’s reported elimination (February 2026) — reflects three converging forces:

– Policy conviction at the highest levels of MoD that monopolistic nomination-based procurement must end, driven by decades of delay across HAL-led programmes.

– Private sector maturation — companies like TASL (already manufacturing the C-295), L&T (submarine and missile systems), and Bharat Forge (artillery and munitions) now possess credible, if untested, ambitions for aerospace integration.

– Strategic urgency — with the IAF’s squadron strength critically below the sanctioned 42 (currently around 31–32) and China deploying J-20s operationally — India cannot afford another decade-long delay on its only indigenous fifth-generation programme.

Whether the private sector can actually deliver a fifth-generation stealth fighter prototype within eight years — without HAL’s institutional memory of fighter aircraft integration — remains the programme’s central risk. The answer will determine whether this model becomes the template for India’s future defence industrial policy, or a cautionary tale about prioritising competition over capability.

***